Know Your Customer (KYC) processes have undergone a transformative journey in the insurance and finance sector, becoming a robust defence in battling fraud. In this blog we explore how and where technological advancements and regulatory imperatives have reshaped the landscape.

Streamlining Processes with Technology

Historically, KYC was synonymous with paperwork and manual verifications, burdening both customers and financial institutions. However, the adoption of electronic identity verification (eIDV) technologies marked a pivotal shift. Automated systems, driven by artificial intelligence and machine learning, now enable real-time identity verification, reducing processing times and minimising human error. Some real time ID verification solutions can provide results in seconds and even help with 10% uplifts by onboarding thin-file clients (credit/ID poor people) that were previously rejected.

Biometric authentication has further strengthened the KYC process. Fingerprint scans, facial recognition, and voice authentication not only enhance accuracy but also make it significantly more challenging for fraudsters to manipulate or forge identities. A prominent financial institution reported a remarkable 90% reduction in identity fraud cases after implementing biometric authentication.

Data Analytics as a Game-Changer

The integration of data analytics into KYC procedures has empowered financial institutions to scrutinise vast datasets. Predictive analytics and machine learning algorithms such as Precision identify patterns and anomalies, allowing for the early detection and prevention of fraudulent activities. Predictive analytics solutions can improve onboarding by 50% and reduce fraud by up to 30%. This proactive approach has saved institutions and customers from potential losses and enhanced the overall security of the financial ecosystem.

Regulatory Drivers of KYC Evolution

Regulatory bodies worldwide have played a pivotal role in driving KYC evolution. Stringent regulations, such as Anti-Money Laundering (AML) directives and the General Data Protection Regulation (GDPR), compel institutions to fortify their KYC protocols. Compliance with these regulations is not only a legal requirement but also a strategic imperative for maintaining trust and safeguarding reputation.

KYC in the Insurance Sector

In the insurance sector, KYC has become a linchpin in combating fraudulent claims. With fraudulent claims costing the industry billions annually, advanced analytics and machine learning algorithms scrutinise claims data to identify patterns indicative of fraudulent activities. One insurance company reported a 30% reduction in fraudulent claims after implementing a robust KYC system.

Challenges and Continuous Innovation

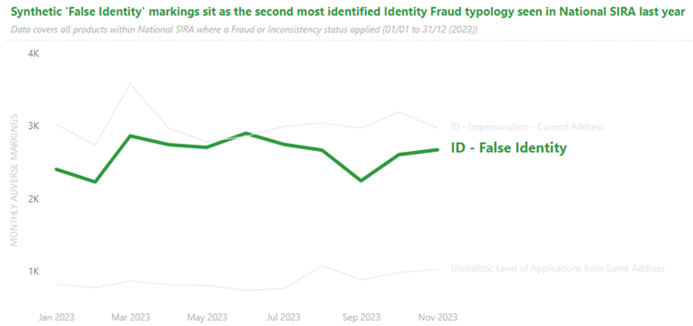

Despite the strides made, challenges persist. The rise of synthetic identities, where fraudsters combine real and fake information to create new identities, poses a significant threat. As per National SIRA, false identities have been the second most identified fraud typology last year.

Continuous innovation and adaptation are essential to stay ahead of fraudsters and secure the evolving financial landscape.

In conclusion, the evolution of KYC in insurance and finance is a testament to the industry's commitment to combating fraud. From manual processes to innovative technologies, KYC has become a dynamic, adaptive force. As a counter fraud specialist, we remain optimistic about the future, where ongoing technological advancements and collaborative efforts will further fortify KYC as a formidable defence against financial fraud.